NVIDIA Corp logo on the phone and AI chip, by Below the Sky via Shutterstock

Nvidia (NVDA) is a global technology leader specializing in graphics processing units (GPUs), data center hardware and artificial intelligence solutions. The company’s GPUs power everything from gaming and creative workstations to cloud computing, autonomous vehicles, and AI-powered data centers. Nvidia’s advances in GPU-accelerated computing and its CUDA software platform have been instrumental in advancing high-performance computing and artificial intelligence across industries.

Founded in 1993 and led by Jensen Huang, Nvidia is headquartered in Santa Clara, California. The company operates in 38 countries with an estimated 92% market share in the discrete GPU market.

About Nvidia Stock

Nvidia stock has shown strong performance through 2025 despite recent volatility. Despite falling a combined 5% on Monday and Tuesday, over the past five days, NVDA stock has risen 4% and has shown further resilience in the one-month period, where it is up more than 6%. Over the six-month period, Nvidia has gained 44%, driven by strong demand. Its 52-week performance represents a gain of 33%, while the stock is 8% below its 52-week high of $212.19 set on October 29.

The AI company has outperformed the illustrious S&P 500 ($SPX), which is up 14% in the same time and also up 14% in the last six months.

www.barchart.com

Nvidia surprises with third quarter results

Nvidia reported third-quarter fiscal 2026 results on Nov. 19, generating $57 billion in revenue, beating analyst estimates of $55.2 billion. Adjusted earnings per share were $1.30, also beating the consensus estimate of $1.26. The strong top-line and bottom-line outperformance was attributed to persistent strength in AI demand, continued cloud and data center growth, and broad customer adoption across enterprise and hyperscale segments.

The company achieved healthy margins, with a gross margin of over 71%. Free cash flow remained exceptionally strong due to increased data center sales, while Nvidia’s cash reserve reached an estimated $40 billion at the end of the quarter, supporting aggressive R&D and capital return plans. The core data center segment led revenue, growing nearly 80% year-on-year, and AI chip sales set a new record. Nvidia’s operating income increased and shareholder returns remained high thanks to continued buybacks and dividends. Key performance metrics included accelerated adoption of Blackwell-class GPU platforms and new achievements in large AI infrastructure deployments.

Looking ahead to the fourth quarter of fiscal 2026, Nvidia provided strong guidance, forecasting $65 billion in revenue, well above the Wall Street consensus of $62 billion, and continued strong demand for its AI chips and system solutions. Management sees positive momentum in the AI and cloud markets, guiding it to maintain elevated margins and emphasizing “off-the-charts” demand for next-generation Blackwell chips, positioning Nvidia for another record quarter.

JP Morgan warns of AI correction

Daniel Pinto, vice president at JP Morgan Chase, warned that valuations in the burgeoning AI industry are likely due for a correction that could significantly impact the AI sector and ripple through the entire stock market, including the S&P 500. Pinto noted that current market valuations assume rapid productivity gains from AI technologies, which may not materialize as quickly as expected, prompting a reassessment. While he does not foresee a recession in the United States, Pinto anticipates slower economic growth and limited improvement in stocks in 2026.

Supporting this caution, a report from McKinsey & Co. highlights that tech giants will spend approximately $371 billion on data centers in 2025 alone to support AI workloads, and this scale of infrastructure spending is projected to reach $5.2 trillion by the end of the decade. This massive investment underpins the growth of the AI market, but also fuels valuation concerns about whether the returns will justify the costs within the expected timeframes.

This balanced outlook suggests investors should remain cautious amid the current optimism, as the degree and pace of AI-driven productivity and earnings growth may face challenges, even as companies like Nvidia continue to beat analysts’ earnings expectations thanks to strong demand for AI.

Should You Buy NVDA Stock?

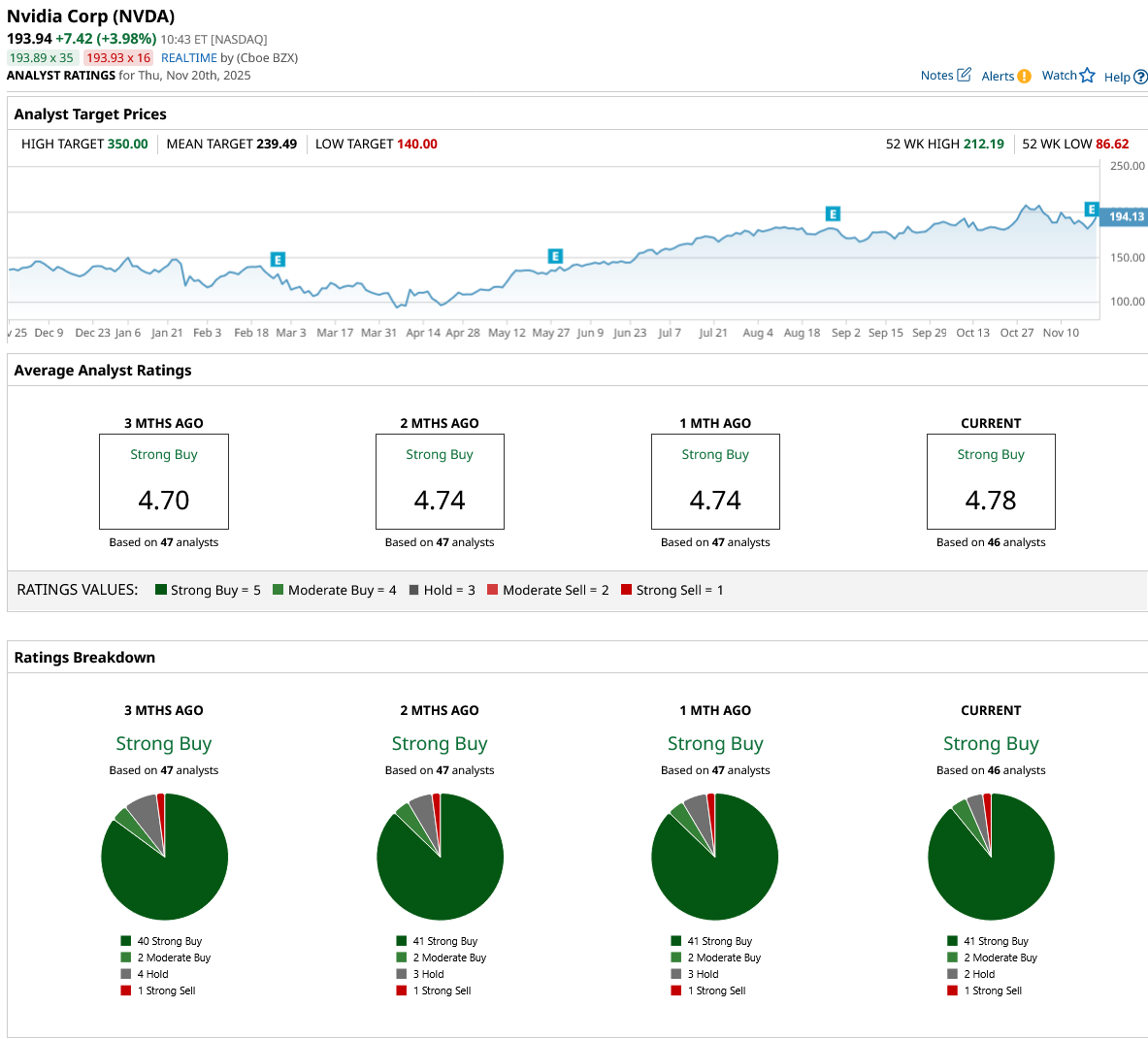

Nvidia is currently up 4% in early market trading following its results last night. NVDA stock has been a clear buy, with market experts saying it has a “Strong Buy” consensus rating and an average price target of $239.49, reflecting a 24% upside potential from the market rate.

The stock has been studied by 46 analysts with 41 “Strong Buy” ratings, two “Moderate Buy” ratings, two “Hold” ratings and one “Strong Sell” rating.

www.barchart.com

On the date of publication, Ruchi Gupta had no (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article are for informational purposes only. For more information, see Barchart’s Disclosure Policy here.