Lam Research Corp_ HQ signed by Michael Vi via Shutterstock

Lam Research Corporation (LRCX) is a leading semiconductor equipment company specializing in the design, manufacturing and maintenance of wafer processing systems for integrated circuit manufacturing. Based in Fremont, California, it provides crucial tools used in deposition, etching, cleaning and other initial and final steps of wafer processing. Lam Research’s market capitalization is around $187.6 billion, making it one of the most valuable players in the semiconductor equipment space.

Shares of the semiconductor giant have outperformed the broader market. Over the past 52 weeks, LRCX stock has gained 112.1%, while the broader S&P 500 index ($SPX) has gained 12.3%. Additionally, year-to-date (YTD), the stock is up 106%, compared to SPX’s 12.9% return.

Zooming in closer, LRCX’s outperformance is also evident compared to the First Trust Nasdaq Semiconductor ETF’s (FTXL) 35% rise over the past 52 weeks and 34.8% year-to-date rise.

www.barchart.com

Lam Research shares have risen strongly in 2025, driven by growing demand for data center and artificial intelligence (AI)-focused chips. As more companies invest in high-performance computing, the need for advanced wafer manufacturing tools like those Lam produces for deposition and etching has skyrocketed. On top of that, favorable macroeconomic tailwinds, such as proposed tax credits to boost U.S. chip manufacturing, are further strengthening its growth prospects.

For fiscal 2026, which ends in June, analysts expect Lam Research’s EPS to grow 15.7% year-over-year to $4.79. The company’s track record of earnings surprises is promising. It surpassed consensus estimates in each of the last four quarters.

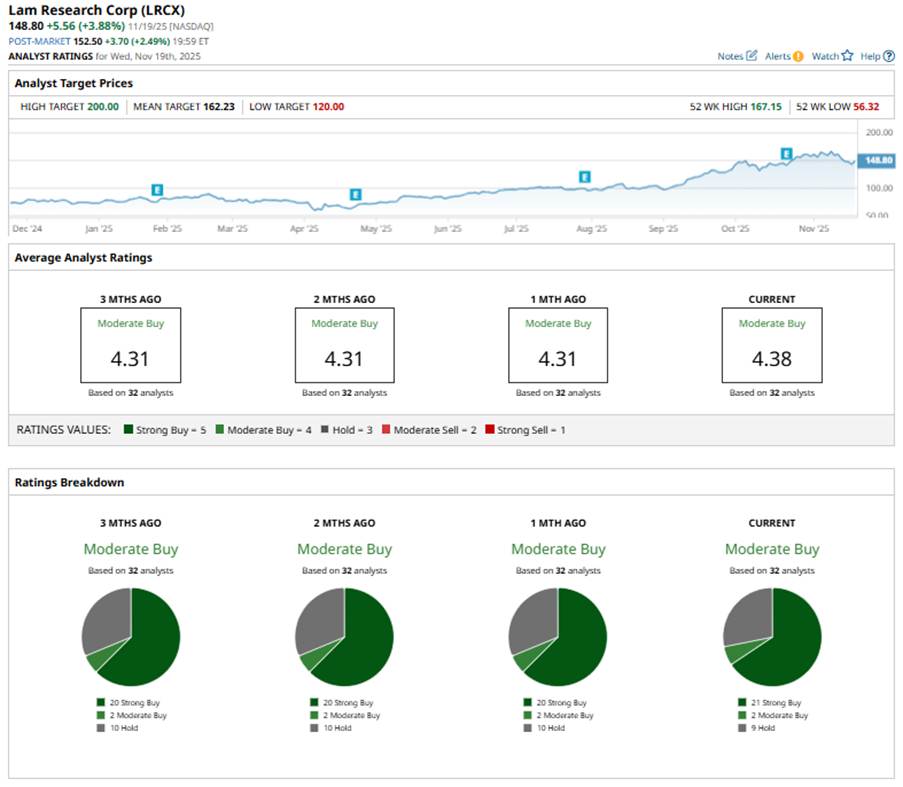

Among the 32 analysts covering the stock, the consensus rating is “Moderate Buy” and is based on 21 “Strong Buy” recommendations, two “Moderate Buys” and nine “Hold” ratings.

www.barchart.com

This setup is slightly more bullish than a month ago, when there were 20 “Strong Buy” ratings.

Last month, TD Cowen raised LRCX’s price target to $170 from $145, maintaining a “Buy” rating, highlighting the company’s strong September quarter, driven by strong Chinese demand for logic and front-end equipment. TD Cowen remains optimistic and expects Lam to benefit from NAND upgrades, growing HBM demand and the strength of leading-edge logic, creating a stronger market heading into 2027.

The average price target of $162.23 represents 9% upside potential, while the Street’s high price target of $200 suggests the stock could rally as much as 34.4% from Wednesday’s close.

On the date of publication, Sristi Jayaswal had no positions (either directly or indirectly) in any of the securities mentioned in this article. All information and data in this article are for informational purposes only. For more information, see Barchart’s Disclosure Policy here.